Published: April 28, 2010

By Jim Lichtman

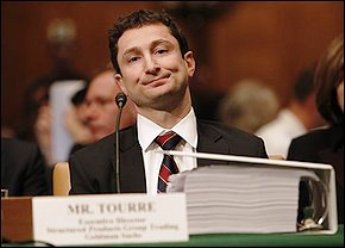

You’d look like this too, if you had to sit before Chairman Carl Levin and the Senate’s Permanent Subcommittee on Investigations looking into alleged improprieties of investments and investment procedures by Wall Street banking and investment giant Goldman Sachs. Get a load of the document bundle sitting in front of (self-named) “Fabulous Fab” Fabrice Tourre, the architect of the investment vehicle under SEC scrutiny.

Trying to understand the Goldman executive’s explanations of these high-level security instruments reminded me of the Gary Larson cartoon: “What We Say to Dogs, ‘Okay, Ginger, I’ve had it! You stay out of the garbage! Okay, Ginger, or else!’; and “What Dogs Hear: “blah, blah, Ginger blah, blah, blah, blah, Ginger, blah, blah!”

Here are some of my notes from yesterday’s marathon session that wrapped up around 5:45pm (PST):

Chairman Levin: “Goldman often saw its clients not as customers but as objects of profit.”

Sen. Claire McCaskill: “You all are the house, you’re the bookie… [Clients] “are booking their bets with you. I don’t know why we need to dress it up. It’s a bet…You have less oversight than a pit boss in Las Vegas.”

Sen. Susan Collins: “Do you have the duty to act in the best interests of your clients?”

Fabrice Tourre: “I believe I have a duty to serve my clients.”

When faced with a series of questions about e-mails, financial products and decision-making, many of the questions by committee members were met with responses like these:

“I don’t know,” “I did not participate in those deals,” “I don’t recall,” or “I left to spend more time with my family.”

The only excuse not used: “The dog ate my investment guidelines!”

In the afternoon session, Senator Mark Pryer said, “I’m going to ask all of you the same question: Do you think your actions and Goldman’s actions contributed to the economic downturn in 2008?”

Each of the four, former Goldman officials believed that they did nothing wrong. However, former Goldman executive Dan Sparks said that it sounded like Pryor was asking him if he had any regrets, and said: “Regret to me is when you feel bad about something you did wrong and I don’t feel that. We made mistakes.”

Pryor persisted, “Did Goldman contribute to the downturn?”

“I don’t know, Sparks said. “I would like to think about that.” A little more thinking and Sparks added, “It’s clear that credit standards overall got loose,” he said. “Too loose. There were assumptions made and I think risk overall wasn’t respected across the industry and we participated in that industry. I’m not trying to avoid your question, senator. I mentioned my feelings about what I did and I don’t have regrets…But we participated in an industry that got loose.”

I lost count of the times the words ethics, ethical standards or code of ethics came up, but not a single Goldman executive was willing to clarify exactly what those standards are.

Here are some of the questions I would have asked:

1. Could you tell us about Goldman’s ethics training?

2. Could you offer an example where you utilized Goldman’sethical standards?

3. Could you explain how any Goldman manager utilized ethical decision-making in selling financial products?

4. In light of the financial crisis, what kinds of changes toGoldman’s ethics policy would you recommend?

At the end of the hearing Goldman CEO Lloyd Blankfein made clear, “Our client’s trust is not only important to us, it is essential to us.”

My question for Mr. Blankfein: How do you maintain that trust in “an industry that got loose,” and a firm that “made some poor business decisions,” as Sparks said earlier.

I don’t mind people making money, even making a lot of money. I draw the line at making any money on the backs of hardworking investors who ended up losing billions.

Anyone out there who does not think that Wall Street is overdue for major regulatory overall please send me your reasoning. I’ll post your comments.

Comments

Recent Commentaries

All the President’s Men 2.0

July 23, 2026

The Threat to November Is Already Here

July 20, 2026

Jon Ossoff and the Conscience of Atticus Finch

July 17, 2026

Hearts and Minds

July 16, 2026

The Ethics of Belonging

July 14, 2026

The Best of Us

July 9, 2026

The Standard Washington Set

July 6, 2026

Who We Were. Who We Are…

July 4, 2026

Are We Still Worthy of What They Declared?

July 3, 2026

Are We Still Worthy of What They Declared?

July 1, 2026

Read More Articles

The Latest... And Sometimes Greatest

Are We Still Worthy of What They Declared?

For the most part, my high school history classes consisted of names, dates, documents, and battles. What I’ve learned since then — through historians like...

June 29, 2026

A Cautionary Tale: France Then, Washington Now

Lately, I’ve been reading more history, mostly to educate myself. But the other night, I opened Lord Acton’s Lectures on the French Revolution and didn’t...

June 25, 2026

Different Issues. Same Fear.

As our nation nears its 250th anniversary, an uneasy emotional connection to the past has returned—one rooted in fear, and the question of who gets...

June 22, 2026

When Democracy Comes Dressed as Patriotism

The current American political order is starting to feel like a collision between the films Seven Days in May and All the King’s Men. One...

June 18, 2026

Who Watches the Algorithm?

We are building machines that may soon judge, persuade, police, diagnose, hire, fire, and even help governments decide whom to trust. Yet we still have...

June 15, 2026

He Just Does His Job

I’ve been listening to and watching Democratic Senator Jon Ossoff of Georgia for more than a year now: his speeches, his questions in Senate hearings,...

June 11, 2026